When you’re self-employed, getting on top of your taxes is really important. Not only are they dreaded by newbie (and even long-time experienced) freelancers, but they can be pretty stressful if you leave them to the last minute. That’s why at TaxScouts, we have a few recommendations that will help you get on top of everything. Your tax return does not need to be an annual event of doom and gloom.

Learn how tax works

This is important. Once you know the basic structure of how we’re taxed in the UK, it’s easier to get your head around everything else.

The tax year runs from 6th April to 5th April over any given two-year period. What you earn each year between these two dates is the income you’ll be taxed on. For example, in the 2020/21 tax year, you’ll need to calculate tax on your earnings between 6th April 2020 - 5th April 2021.

Understand what you owe

When you’re self-employed, there are two types of tax that you might be liable to pay:

- Income Tax

- National Insurance

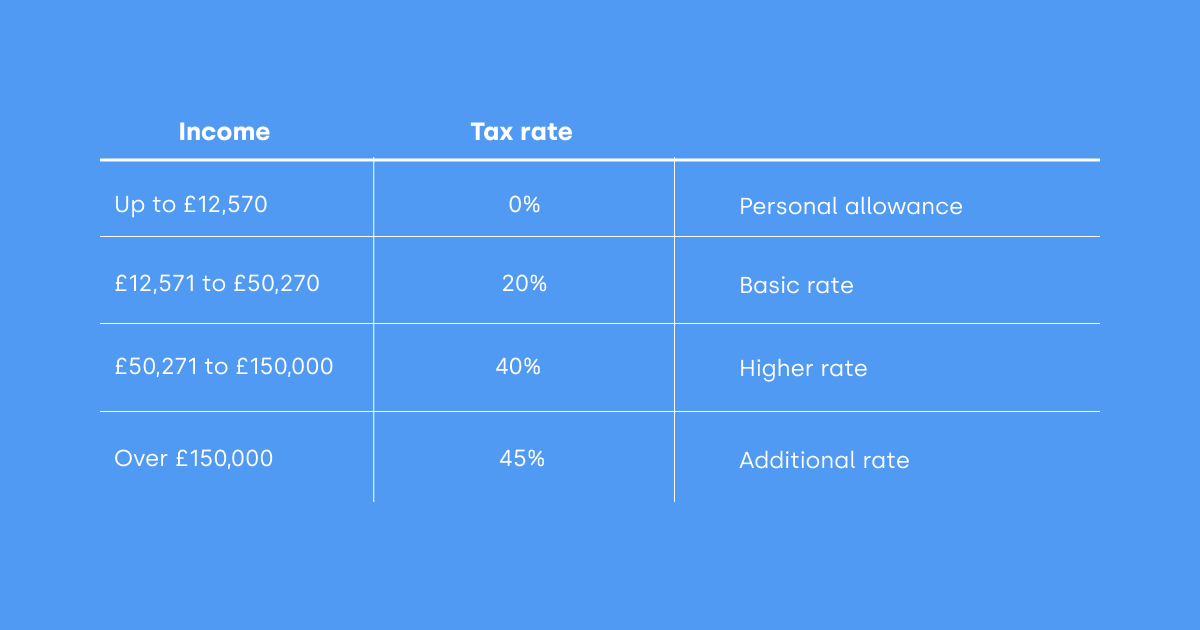

We all have to pay Income Tax, whether we’re employed or self-employed. What we pay is based on how much we earn. Take a look at the below table to see how much you’ll owe based on your earnings. Or if you’re based in Scotland, click here.

When it comes to National Insurance, this works a bit differently. Even if you earn less than the tax-free Personal Allowance, you’ll still be liable to pay it. This is because it entitles you to certain state-provided benefits such as the state pension or the disability allowance. You pay either Class 2 National Insurance (if you earn over £6,515) or Class 4 National insurance (if you earn over £9,568). If you’re employed, you pay Class 1 National Insurance.

Diarise the deadlines

As you can probably imagine, there’s quite a lot of admin involved in doing your taxes. One part of this is learning the dreaded deadlines. There are a few to get in the diary to stay on top of things:

- Register for Self Assessment - 5th October

- Tax return deadline - 31st January

- Payment on Account deadline (when you pay the second half of your tax bill) - 31st July

Get to know the worst-case scenario

And by this, we mean the penalties. When you don’t meet the above deadlines, HMRC will penalize you. And the longer you leave it, the more you’ll be liable to pay. It’s important to remember though that the more transparent you are with HMRC, the more lenient they’ll be. Head over to the TaxScouts site to use our late payment calculator so that you can prepare for the worst (but hope for the best/motivate yourself to not pay late!).

Stay organized

However you feel about spreadsheets, they are your friend when it comes to keeping your financial affairs in order. We’d recommend doing the following bits to keep on top of things:

- Open a business account to keep your personal and business spending separate

- Create spreadsheets at the start of each tax year

- Track as you go

- Split your spreadsheets into monthly tabs and record your income and expenses

- If you do leave your taxes to the last minute (we’re all human, ey?), go through your bank statement with a highlighter to make sure to record everything

Be aware of expenses

Expenses seem to cause a lot of confusion for the newly self-employed. Basically, when you’re self-employed and pay your own taxes, HMRC allows you to deduct any business spending from your overall income. That way, you’re only taxed on your profits. Expenses can be anything that you spend wholly, exclusively, and necessarily on your business. That can be anything from an office chair to a coffee with a client. You just need to keep the evidence of your spend.

Read more about what you can and can’t expense here.

Don’t forget about tax reliefs

Did you know that over £20 billion worth of tax refunds and reliefs are left unclaimed? That’s why as well as knowing what expenses you can deduct, it's a good idea to get an understanding of what tax reliefs are available. They can really help you to become more tax-efficient by reducing what you’re liable to pay. Here are a few examples:

- Tax relief on private pensions contributions

- Gift Aid relief

- Maternity Allowance

- Mileage Allowance

- And more!

Want to learn more?

Sign up to TaxScouts today and we’ll not only do your tax return fast, online, and at super-low cost, but we’re here to help you every step of the way, making your tax return as cool and chilled as the celebratory drink you’ll have once it’s been filed.