Artikel

4 min read

Labo(u)r market roundup: March 2026

Author

Lauren Thomas

Published

March 25, 2026

On both sides of the Atlantic, the job market is slowly deteriorating, although the decline feels more obvious in the U.K., whereas the U.S. is more up and down each month. There are a few bright spots, though: unemployment and layoffs are still relatively low, and the decline in job openings that has plagued us since 2022 seems to have finally smoothed out.

U.S.

The U.S.’s JOLTs and Employment Situation reports were delayed by the partial government shutdown over the past month (this particular line is really starting to feel like Groundhog Day). Not much has changed this month - it’s still the picture of a low-hire, low-fire market, albeit one that may be seeing a turnaround in vacancies.

Hires and quits in January didn’t change very much from December, at 5.3 million and 3.1 million, respectively. Similarly, January’s job openings only slightly changed at 6.9 million. Job openings haven’t changed very much for the past year – but after rapid year-on-year declines between 2022 and 2025, that’s probably good news. Hiring and openings are a leading indicator: the job market right now is pretty frozen, but at least the hiring situation isn’t getting worse.

Layoffs remained constant at 1.631 million, down very slightly from 1.666 million in December. The layoff rate of 1.0% is still pretty low compared to what we saw in the Great Financial Crisis, where layoffs reached 2.0% and mostly remained above 1.3% until 2016.

Payroll employment shrank by 92,000 in February, a surprise after a strong January. As my old boss and Glassdoor Chief Economist Daniel Zhao pointed out on LinkedIn, workers have seen a job market that has alternated between job losses and job gains since May 2025. Healthcare saw a decline, although much of that is due to strikes and should reverse in the next months. Even without the strike, healthcare still did not have a strong month – this could be worrying if it becomes a trend, as it’s provided much of the job gains over the last year.

My view: I expect healthcare to recover and continue to add more jobs. The underlying structural forces – most notably an ageing population, but also a labor-intensive model that captures the surplus of productivity gains from other sectors to fund more advanced care – are just too strong to resist.

A bright spot: unemployment remains low at 4.4%. This is less than half what it was at its GFC peak in April of 2009 and similar to the job market of late 2017. While it’s been ticking up over the last three years, the rate of growth has slowed over the last month.

Finally, average hourly earnings increased by 3.8%. Though down from the 4.1% growth rate in February 2025, this is a lot higher than the 2-3% growth rates that were the norm before the pandemic. Of course, so is inflation, so workers aren’t feeling that as much as we might like.

U.K.

The third U.K. job market report of the year, which came out today, has reinforced the noticeable year-over-year decline we saw in February.

Real wage growth has continued to fall, at only 0.5% year-on-year. That’s despite abnormally high nominal pay growth (3.8% year-on-year): inflation continues to take its bite.

While job vacancies fell by 6,000 from the last quarter, it’s clear that the curve is flattening. Interestingly, I’m seeing a lot of similarities with the US labour market here: the fall in vacancies has slowed massively to the point where changes month-to-month are nearly flat. This is good news for the British labour market.

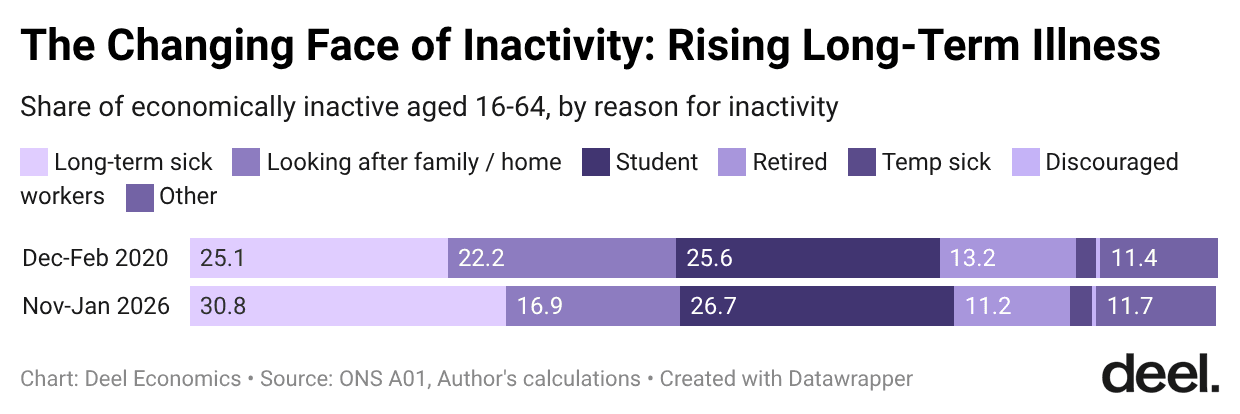

Both unemployment and employment are up from a year ago. At 5.2%, unemployment is very clearly rising. Youth (those aged 18-24) unemployment over the last quarter is up to 14.5% – that's up from 12.9% a year ago. The good news is that economic inactivity for those aged 16-64 is falling and is now back to pre-pandemic norms.

However, the makeup looks pretty different from pre-covid: the vast majority of this fall has been driven by a decline in those looking after their family, which is down 6.6% from last year. In the quarter leading up to the pandemic, 22.2% of economically inactive 16-64 year olds were inactive due to looking after their family or home; 13.2% were inactive due to early retirement, 25.6% due to being a student, 25.1% due to long-term illness, and 2.5% for other reasons. In the most recent quarter, only 16.9% are inactive due to family reasons, while an astounding 30.8% are inactive due to long-term illness.

This is a major composition shift and has real implications for the public purse: those on long-term disability are almost certainly more likely to be supported by benefits and less likely to return to the labour market than those who have exited for family or caregiving reasons.

Data deep dive

This month’s data comes from Deel’s platform. We serve workers from all across the globe, which means we’re able to dive deeper into questions that might not typically be investigated.

In honor of International Women’s Day on March 8, I wanted to investigate whether platforms like Deel can help connect women to jobs in ways that local markets cannot.

There are two opposing forces here: Deel's worker population tends to draw from tech-heavy full-time roles like software developer, which tend to be male-dominated. But past economic research has suggested women have a preference for remote or flexible roles, which are also incredibly common on Deel.

Because roles hired through Deel’s employer of record (EOR) and independent contractor program are almost always remote roles, one might expect to see a relatively higher female population on Deel. So which of these opposing forces wins out?

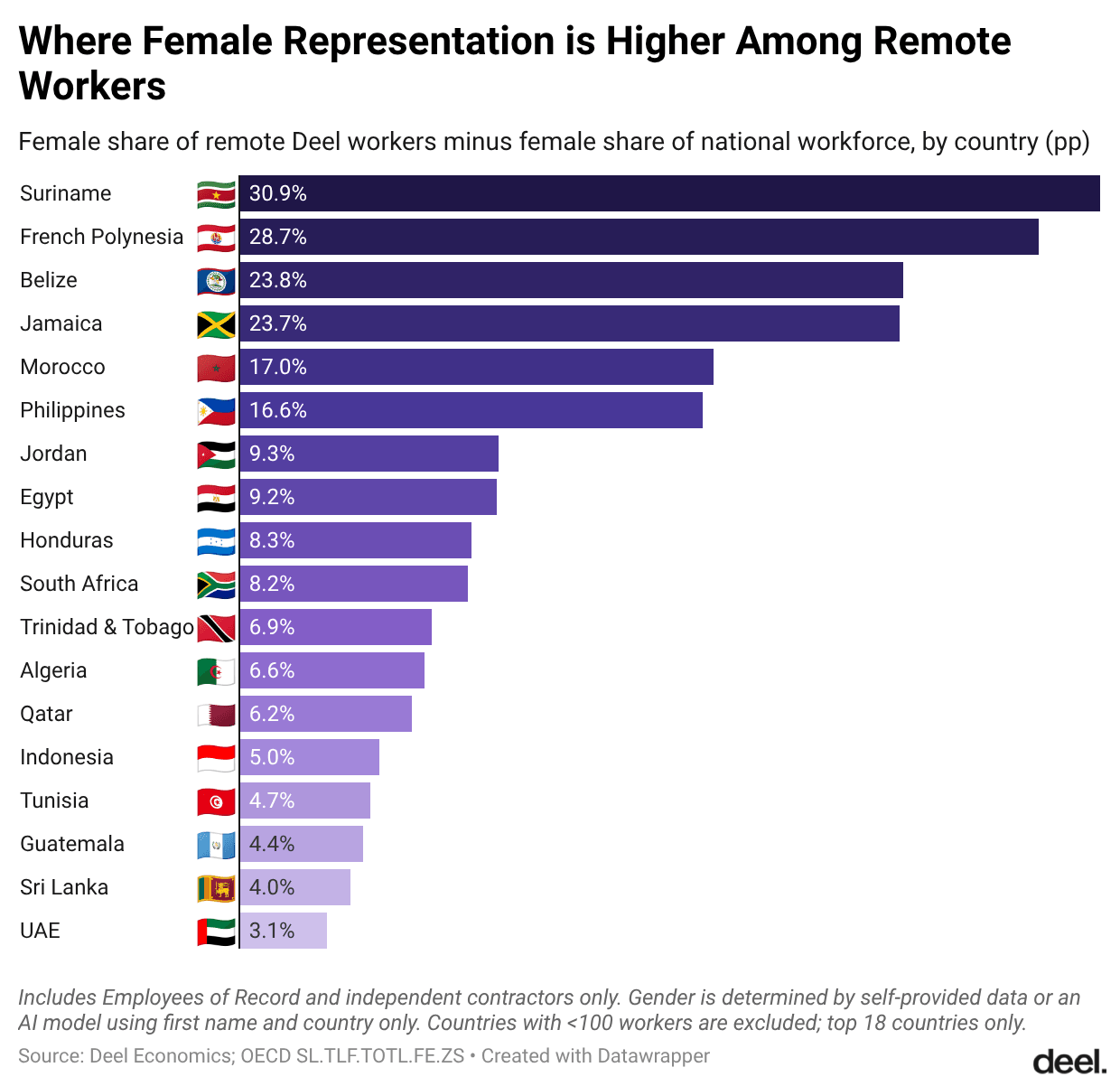

I pulled the countries where the gap between the share of Deel EOR and IC employees who are female and the share of the overall population that is female (the latter sourced from OECD data) is highest.

In this list, we see mostly countries with heavily male-dominated workforces; women make up about a third or less of the workforce in 11 of these places: Morocco, Jordan, Egypt, Honduras, Algeria, Qatar, Sri Lanka, Tunisia, Guatemala, Sri Lanka, and the UAE. You can see this in Chart 2, which maps the global workforce by share that is female.

Lauren Thomas is Deel's founding Economist, where she’s helping to bring Deel’s mission of breaking down geographic barriers to opportunity to life through data — a mission that resonates personally, as she's worked and studied in six cities across three countries!

Before joining Deel, Lauren worked in economic research and data storytelling at the Federal Reserve Bank of New York, Glassdoor, and Stripe. She has degrees in economics and data science from Oxford, Université Lumière Lyon 2, and Northwestern University.

Outside of work, she enjoys reading, playing volleyball, climbing, sewing her own clothes, and using Oxford commas. She does not enjoy long flights but takes a lot of them anyway!