Article

7 min read

Labo(u)r market roundup: February 2026

Author

Lauren Thomas

Published

February 18, 2026

While the low-fire, low-hire market remains the dominant narrative of both countries’ job reports, I’m starting to see a potential divergence between the markets. Unemployment rates have risen by 18% in the U.K. but only 7.5% in the U.S. During times of economic distress, the U.S. has historically had lower unemployment rates than European countries, despite (and, indeed, perhaps thanks to) looser labour laws on that side of the pond. Will unemployment continue to rise?

U.S.

The U.S.’s JOLTS and Employment Situation reports were delayed by the brief government shutdown this month, eventually coming out a few days late.

The overall report was surprisingly positive, though many of the headlines focused on the annual data revisions to payroll data. Monthly payroll counts depend on surveys, which have quick turnaround times but are more inaccurate. The yearly benchmark revision relies on more accurate administrative data from the states. These revisions downgraded the number of jobs added for every month in 2025, taking it from +584k to +181k for all of 2025. That’s obviously a big drop!

Total non-farm payroll employment rose by 130,000 in January, with the bulk of job gains coming from health care, social assistance, and construction. I expect to see the first two categories continuing to provide the bulk of job gains for the rest of this year - and likely for years to come. Health care takes years to train for and is highly regulated, is only going to grow in importance as the population ages, and has proven consistently difficult to automate. Those factors mean that it's going to remain an in-demand field.

Unemployment changed little from December, ticking down 0.1 pp to 4.3%. That's up from 4.0% a year ago. Labor force participation remains sluggish at 62.5%. This dropped hugely post-COVID and has never really recovered fully. With an aging population, I don't expect it to.

With that said, I'm seeing some consistent pockets of concern. Two figures that stood out to me in today's report:

The number of people unemployed because they're new entrants to the labor market has increased by 18% since last year. New entrants (mostly high school and college grads) are making up a larger proportion of the total unemployed than they used to.

Over the last two years, the number of those who have been unemployed for 6 months or more has grown faster than any other unemployment category, from 1.279 million in January '24 to 1.835 million last month. This group has gone from 20.7% to 25% of all unemployed people in that time. And as the BLS's chart below shows, that figure is headed in the wrong direction.

These figures reinforce the narrative that the job market is currently low-hire and low-fire. The job market isn't too bad if you're already employed...but it's a bad time to be looking for something new.

U.K.

The second U.K. job market report of the year, which came out today, has reinforced the noticeable year-over-year decline we saw in January.

First, the bad news: unemployment rates have continued their climb to hit a five-year high of 5.2% in October-December 2025, up from 4.4% a year ago. And similarly to January’s report, involuntary redundancies have also risen to 4.9 per 1000 employees, from 3.9 a year ago. Doctors’ strikes in December helped drive an estimated 118,000 days lost due to labour disputes – the highest since January 2024, next to last month’s 155,000.

Though average weekly earnings remain well above pre-pandemic norms, up 4.2% from a year ago, much of this wage growth has been driven by (and likely partly driving) persistent high inflation. Real (CPIH-adjusted) earnings have only grown by 0.5% over the last year.

In a spot of good news, quarter-on-quarter vacancies increased very slightly, up 2,000 from the quarter before. While they’re down 73,000 from a year before, there’s been a clear slowdown in the job vacancy loss that has persisted since vacancies hit their peak in the spring of 2022. After the rapid falls over the past 3.5 years, this is a good thing.

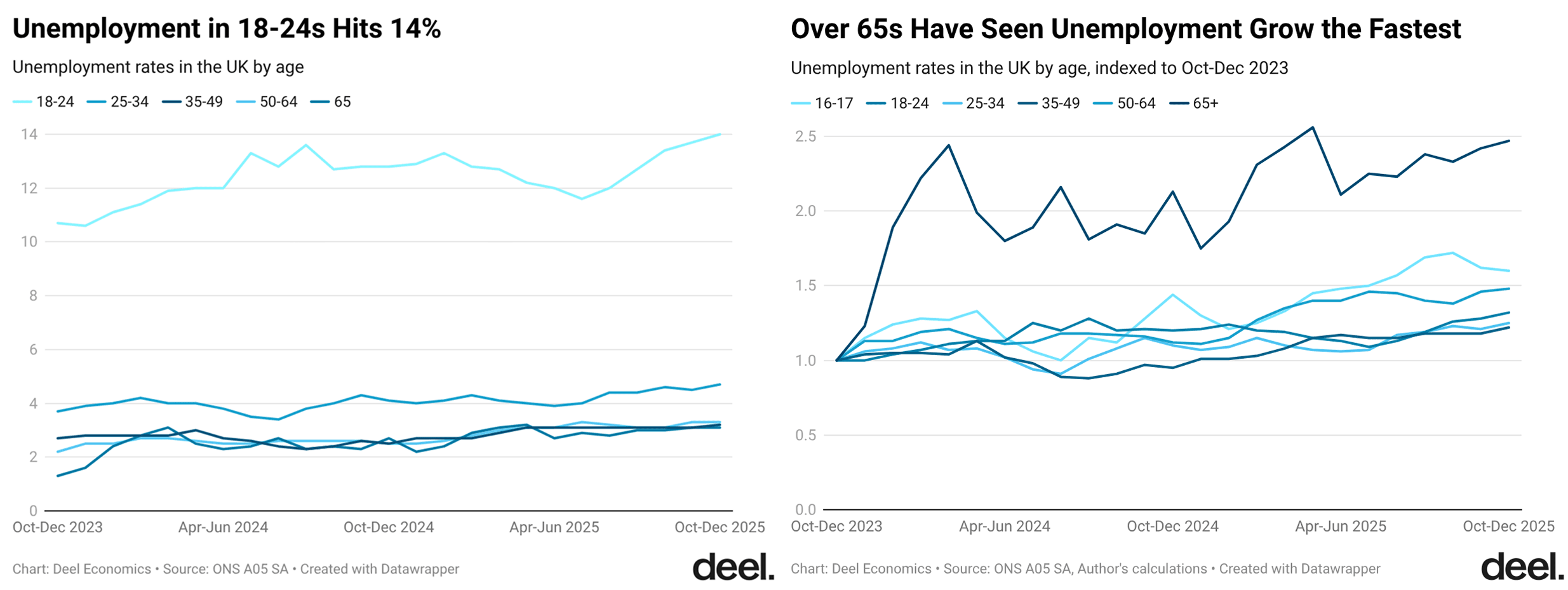

Lastly, something that’s gone mostly unremarked upon…though adult unemployment has risen amongst all age groups and is highest for 18-24 year olds, it’s actually the over 65s that have seen unemployment rates rise quicker over the past two years (see the charts below). A lot of this appears to be driven by a fall in labour market inactivity – almost certainly people either delaying or returning from retirement.

We don’t have the data to say with certainty why this is occurring, but it could be related to high and persistent inflation over the past few years. Seniors live on fixed incomes, some of which (the state pension) are adjusted for inflation, but others of which are not. Working longer may be an easier way for some cash.

Job openings and hires have been depressed for several years now, but the picture hasn’t been nearly so bad for those already in work. It looks like that could be changing - but time will tell.

Data deep dive

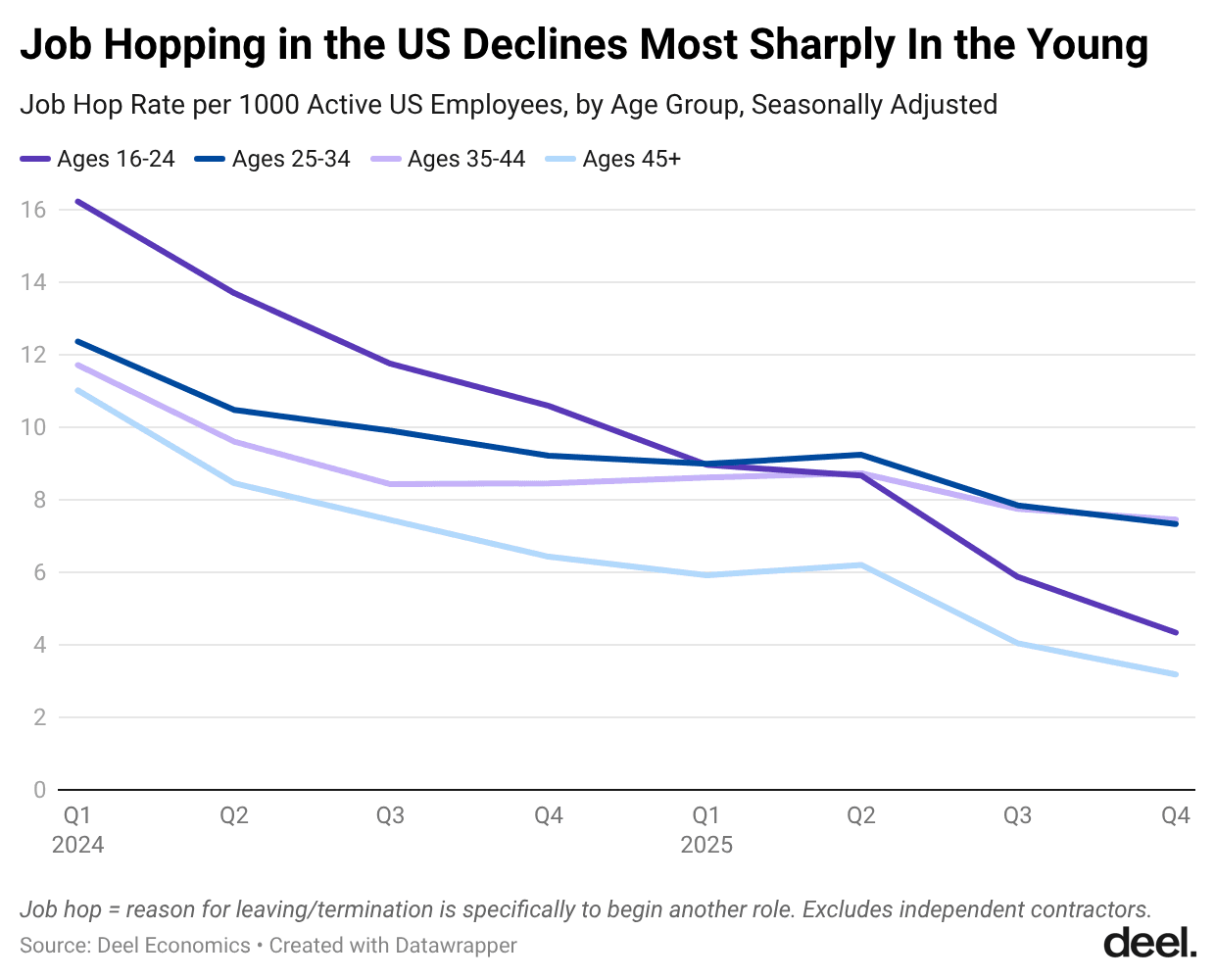

This month’s data comes from Deel’s platform. While the US JOLTS report measures quits (the rate of people voluntarily leaving their jobs), it doesn't specifically measure job-to-job transfers (though, of course, most people quitting are heading to another job). But at Deel, we ask employers to specify why their workers are leaving, and many of them (nearly half) tell us. That means we can look at job hopping rates, or the percentage of active employees in a given quarter who have left their jobs to go to a new one.

That rate has dropped a lot, and it's dropped especially for the very young (16-24). That's unsurprising, considering broader employment trends, but it's still cool to see that reflected in our own data.

Recent labor economics & economics of AI roundup

Below is a sampling of interesting papers and posts on the labor market that I’ve read recently.

Work from home (WFH) and fertility, Nick Bloom (Stanford) et al

Summary: The authors investigated how WFH influenced fertility after the pandemic, using original global and U.S. surveys. By using online job postings data in the U.S., they find that being able to work from home at least one day a week leads to a rise in one-year fertility rates, even after controlling for various confounders. Estimated lifetime fertility is greater by 0.32 children per woman when both partners WFH at least once a week than when neither does.

My view: This is an exciting contribution to the literature on remote work, although I think there is room for more work in this field to rule out selection effects. Though the authors acknowledge this possibility and try to control for it by excluding younger participants, it’s possible that people planning to have children in the next year purposefully look for jobs with some work-from-home opportunities. There’s no doubt in my mind that the two are closely related, though!

AI, Automation, & Expertise, Bouke Klein Teeselink and Daniel Carey (King's College London, AI Objectives Institute)

Summary: The authors extend previous research by exploiting ChatGPT’s use as a natural experiment on the impact of AI exposure on jobs to job listings throughout the world, finding a negative impact of AI exposure on job openings in 31 of 39 countries. This displacement effect seems larger in countries with stricter labor protections and smaller in those with higher digital readiness. They also find that expertise-raising automation raises wages on job listings, whilst expertise-lowering automation does not.

My view: As the authors note, most of the research in this field has been U.S. dominated, so it’s great to see research from elsewhere in the world. I worry about using ChatGPT as a natural experiment: it came out right around the time interest rates started rising, and as a very early adopter, I can tell you it was nowhere near capable of replacing workers (with the possible exception of translators). However, the idea that AI exposure might have worse impacts in countries with stricter labor protections is an interesting one: it reflects another view I’ve seen that employment and innovation may be worse when labor protections are stricter, since companies are less likely to take risks on workers.

Canaries, Interest Rates, and Timing: More on the Recent Drivers of Employment Changes for Young Workers, Erik Brynjolfsson, Bharat Chadar, and Ruyu Chen (Stanford)

Summary: This is a good follow-up from last month’s roundup, where I shared the post by Google’s economists arguing that the downturn in employment attributed to AI is actually an impact of interest rates rises the same year. Brynjolfsson and his coauthors revisit their original Canaries paper, showing that AI-exposed jobs have seen more of a downturn than interest-rate-exposed roles. They also find evidence after controlling for a broader range of factors that the relationship between AI exposure and employment decline starts in 2024, not in late 2022 as their original paper suggested.

My view: I said in last month’s post that I was pretty doubtful that ChatGPT could have replaced workers in 2022. By 2024, AI models were significantly better. I’m not sure which way this debate will turn out, but these results definitely seem more likely than the original ones.

How Do You Identify a Good Manager? Ben Weidmann et al

Abstract: The authors causally identify managerial contributions by randomly assigning managers to lead teams. They find that self-selection into managerial roles is associated with worse outcomes, whereas economic decision making (the ability to consider things like comparative advantages, specialisation of labour, and allocation of scarce resources) and fluid intelligence (the capacity to reason quickly and solve new, unfamiliar problems) in management was associated with better ones. Participants who succeed in the lab receive more real-world promotions and, in a separate study of retail store managers, skill measures strongly predict store sales.

My view: What actually makes a good manager is a hotly contested (and very important) subject. The authors find that good managers make a team ‘more than the sum of its parts’ – which, as someone who has been fortunate enough to have many excellent managers, I absolutely believe. This study is a very cool combination of a strong RCT and an application of the results to the real world.

Lauren Thomas is Deel's founding Economist, where she’s helping to bring Deel’s mission of breaking down geographic barriers to opportunity to life through data — a mission that resonates personally, as she's worked and studied in six cities across three countries!

Before joining Deel, Lauren worked in economic research and data storytelling at the Federal Reserve Bank of New York, Glassdoor, and Stripe. She has degrees in economics and data science from Oxford, Université Lumière Lyon 2, and Northwestern University.

Outside of work, she enjoys reading, playing volleyball, climbing, sewing her own clothes, and using Oxford commas. She does not enjoy long flights but takes a lot of them anyway!